Will it resolve monthly Compliances Ailment?

In India, tax laws have always favoured small businesses as they constitute a major portion of country’s growth and GDP. With the introduction of GST, taxpayers need to file monthly return i.e. GSTR-3B, which comprises of details of outward and inward supplies. Any delay in the filing of return leads to levy of late fees and interest, which is levied on per day basis. This adds to the burden and cost of taxpayers leading to shifting of focus from their core business.

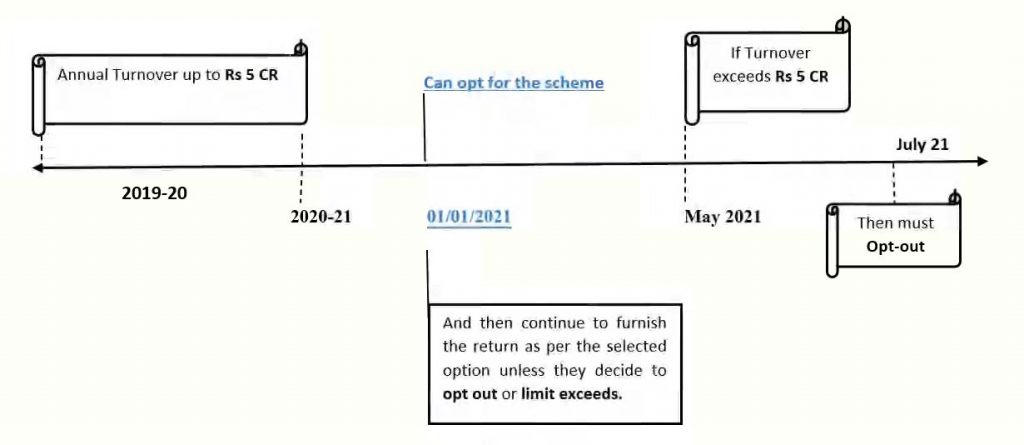

In order to reduce monthly compliance burden and facilitate the ease of doing business, CBIC has notified new QRMP (Quarterly Return Monthly Payment) scheme w.e.f. 1st January 2021 for registered persons having aggregate turnover up to 5 crore rupees opting for quarterly filing of GSTR-3B and monthly payment of tax.

Eligibility– If the aggregate turnover of the taxpayer in F.Y 2019-20 is up to Rs 5 crores, he is eligible to opt for QRMP scheme w.e.f. 01-01-2021. In case the aggregate turnover exceeds Rs 5 crore, say during May 2021, then registered person shall not be eligible for the QRMP scheme from beginning of the next quarter i.e. quarter of July – Sep,2021

When can scheme be opted– A registered person can opt in for the scheme for any quarter from first day of second month of preceding quarter to the last day of the first month of the quarter.

For e.g.- Mr. A want to opt for QRMP scheme from Quarter 2(July-September). In that case, he can apply for the same between 1st May 2021 to 31st July 2021 provided he must have filed the return for the month of June, 2021.

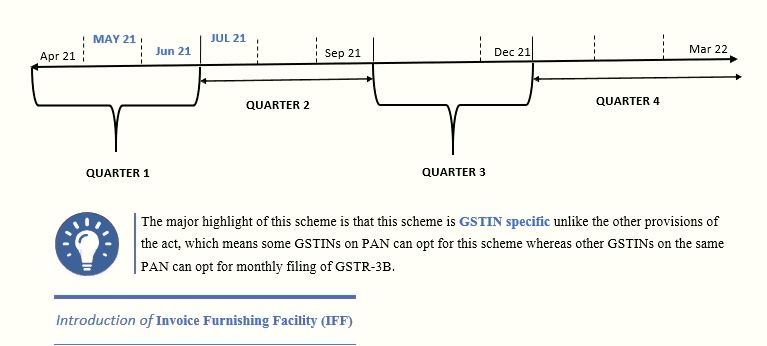

Taxpayers opting for this scheme has the facility of furnishing the details of outward supplies in FORM GSTR-1 quarterly or through IFF-Invoice Furnishing Facility (for each of first and second month of quarter) which is available on common portal from 1st to 13th of the succeeding month.

This IFF facility allows the details of supplies to be duly reflected in form GSTR-2B & GSTR-2A of said recipient thereby enabling them to avail ITC in the same month. However, this facility is not mandatory for the taxpayers and the details furnished in IFF is not required to be reported again in GSTR-1.

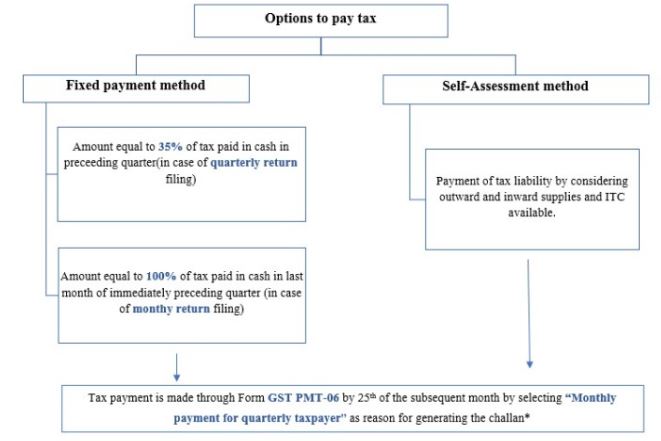

*Any excess amount deposited in cash ledger can be adjusted towards tax liability of subsequent month or can be claimed as refund provided the return of the same quarter has been duly filed.

QRMP is a positive development as it was the first ever initiative towards applicability of provisions on GSTIN basis rather than PAN based. This scheme will act as a tonic for the sufferings faced by the small taxpayers in the form of monthly compliances. Even monthly payment will not prove to be burdensome on taxpayers as they need not worry about late fees or interest liability on delay of filing of returns every month.

This content is meant for information only and should not be considered as an advice or legal opinion, or otherwise. AKGVG & Associates does not intend to advertise its services through this.