With the purpose of enhancing the communicative value of auditor’s report by offering better transparency about audit and providing additional information to the users of financial statements, for the first time, audit reports of listed companies for the Financial year 2018-19 will contain a Key Audit Matters (KAM) as per Standard on Auditing (SA) 701.

Matters that may be reported as KAM

- Impairment;

- Provision for losses;

- Valuation of financial instruments;

- Revenue recognition;

- Taxation Matters etc.

Going concern as a KAM:

-

SA 701 highlights that a material uncertainty related to going concern is, by its nature, a KAM. These matters are to be reported in accordance with SA 570, Going Concern.

-

In the KAM section, reference to the basis of qualified/ adverse opinion or the material uncertainty related to going concern section should be given.

Expected benefits of KAM:

Better governance since it encourages two-way communication between the auditor and TCWG (Those Charged With Governance).

-

Improve overall quality of audits as the auditor would have greater focus on areas requiring careful judgement.

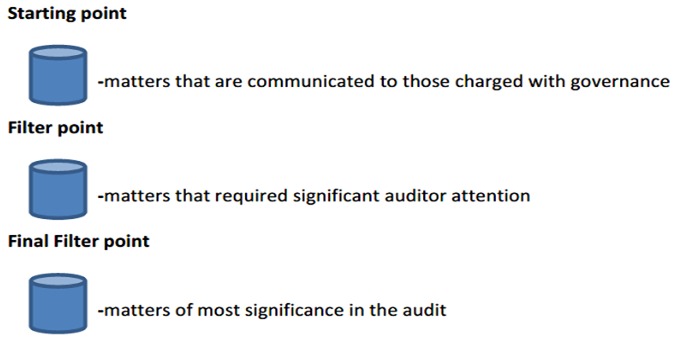

Identification/determination of KAM:

While determining the KAM, which are to be reported in the auditor’s report, the auditor will have to follow filter approach as mentioned below:

Description of KAM

Auditor is required to report in his report a further description of each of KAM by stating that

-Why the matter was one of the most significance in the audit?

-How the matter was addressed in the audit?

Communicating of KAM

There is no limit on the number of matters that can be reported as KAM. A separate section with title “Key Audit Matters” is to be included in the auditor’s report. In this section the language should clearly cover the following:

-

KAM are those matters that in the auditor’s professional judgement, were of the most significant in the audit of the financial statements of the current period; and

-

These matters were addressed in the context of the audit of financial statements as a whole, and in forming the auditor’s opinion thereon, and the auditor does not provide a separate opinion on these matters.

Types of KAMs not to be reported

Under the following circumstances, a matter determined to be a KAM is not required to be communicated in the auditor’s report:

- a) Law or regulation precludes public disclosure about the matter.

- b) The auditor determines that the matter should not be communicated in the auditor’s report.

-

In such a case, a written representation from management, and when appropriate, TCWG(Those Charged With Governance), could be obtained as to why public disclosure about the matter is not appropriate, including management’s view about the significance of the adverse consequences that may arise as a result of such communication.

-

Apart from the above, there could be very limited situations (such as listed entity with very limited operations) where there are no KAMs to be communicated. However, in such a case also, KAM section will be given in the auditor’s report.

Disclaimer: This content is meant for information only and should not be considered as an advice or opinion, or otherwise. AKGVG & Associates does not intend to advertise its services through this.