Any business has always been anchored on accounting. Accounting assists organizations in remaining financially stable, as far as keeping financial records are concerned as well as keeping them tax compliant. Nevertheless, due to the rapid digitalization, companies are currently shifting to AI accounting solutions that can automate most of the conventional accounting processes. Although the classical approaches to accounting still have some value, AI-enabled tools are transforming the way financial management is handled.

The knowledge of the distinction of traditional and AI accounting can make businesses choose which one fits their growth strategy and their business operations.

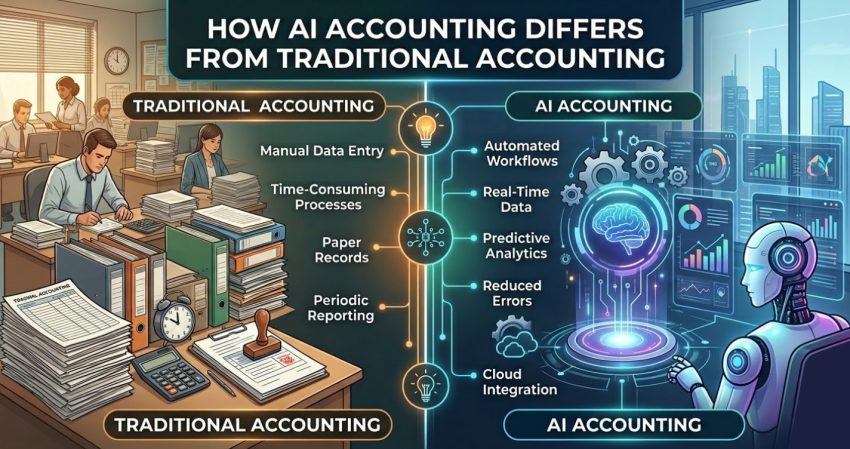

The meaning of traditional Accounting

Mainly, traditional accounting relies on manual data entry, spreadsheet calculations and human verification. Accountants gather financial information, compile reports, balance accounts and see to it that regulatory requirements are adhered to.

Although this is a sure technique, it may be time-consuming and is subject to the error of human beings. In the case of small firms where transactions are limited, then traditional accounting is still effective. Nevertheless, when the transaction volumes grow, it is difficult to maintain records manually.

What Is AI Accounting?

AI accounting is the field in which artificial intelligence, machine learning, and automation are applied to address financial processes. These systems have the capability of automatically classifying transactions, identifying anomalies, producing financial reports and even forecasting the financial trends in the future.

By using AI in accounting, companies can save on the number of manual employees and enhance their accuracy. The system is constantly learning based on patterns of financial data and as time goes by, makes processes faster and more efficient.

Key Differences between AI Accounting and Traditional Accounting

Speed and Efficiency

Traditional accounting has a manual aspect of data processing, which could take hours or days based on the number of transactions. Contrarily, AI accounting is able to handle huge volumes of financial data in a few minutes. This assists the companies in closing books within a shorter time span and real-time financial information.

Precision and Minimization of errors

Manual accounting is usually prone to human error particularly in repetitive activities such as data entry or reconciliation. AI accounting reduces these risks through the process of automation of calculations and verification processes. This leads to better financial reporting.

Cost Management

Conventional accounting is more labor intensive particularly in the case of expanding business. Administrative costs, salaries and training grow as time goes by. AI accounting can help lower operational expenses in the long term because automation of routine activities using AI tools can be costly in the short term.

Fraud Detection and Risk Management

Traditional accounting can only identify fraud once there is a financial review or audit. A system that processes unusual transactions in real time can identify them using AI. Using AI in accounting, companies will have early warnings about suspicious activities that will enable them to avoid losses.

Data Analysis and Prognostication

Traditional accounting deals predominantly with past data. The analysis of financial forecasting is normally done separately. AI accounting has the potential to make business smarter by analyzing trends in the past, and forecasting through the application of AI.

Scalability

Transaction volume increases as an increase in the size of the business. Conventional accounting systems can hardly sustain themselves without increasing their workforce. The accounting system based on AI can be easily scaled and used to work with growing data without any serious add-ons.

Which of the Two Businesses Select?

The decision to use traditional accounting or AI accounting will be based on the size of the business, the volume of its transactions, and its expansion requirements. Traditional accounting could still be adequate for small businesses that have low transactions. Nevertheless, AI accounting automation and predictive analytics are of great value to medium and large businesses.

The hybrid model in which AI tools are used to automate more routine activities and accountants are asked to concentrate on strategy, compliance, and financial planning, are becoming a popular trend in many organizations.

Future of Accounting

The accounting profession is shifting to automation and smart systems. It will not take over accountants but will enrich their abilities. Advisory roles, financial strategy, and compliance management will become a more important concern of the professionals, whereas repetitive tasks will be performed by automation.

With the further development of technologies, AI accounting will be more convenient and affordable not only to large businesses but also for smaller ones.

This content is meant for information only and should not be considered as an advice or legal opinion, or otherwise. AKGVG & Associates does not intend to advertise its services through this.

Also Read: AI Accounting: Understanding the concept