To stop registered persons from generating fake tax invoices and the corresponding recipients from claiming the ITC thereon, the Government of India had come up with the solution of generating E-Invoices. It is a system in which B2B invoices are authenticated electronically by registered persons for further use on the GST portal. Under this system, a unique Invoice Reference Number (IRN) along with a digitally signed QR code containing the details of the invoice is issued against every invoice by the Invoice Registration Portal (IRP).

Interoperability and seamless exchange of data, for not only the Government but also for the businesses, is often the underneath reason for the implementation of standards like E-Invoicing.

While the major discussions and upgrades for the E-Invoicing system are seen from supplier’s and outward sales perspectives, the impact on the inward supply invoices i.e., the purchase cycle also needs attention.

Impact of E-Invoices on the purchase cycle

Recipient claiming Input Tax Credit (ITC)for an invoice supplied by a person who is required to comply with the E-Invoicing provisions should necessarily check that the invoice must contain IRN and QR code. Therefore, a tax invoice will be considered valid when the IRN and QR code is generated for the same.

The Government of India has also provided facilitation to check whether a registered person is required to generate E-invoice or not, the same can be accessed at https://einvoice1.gst.gov.in/Others/EinvEnabled

Advantages of E-Invoicing to be leveraged for the purchase cycle

The procedure of IRN generation must be completed by the vendor or supplier who issued the invoice. Another significant benefit of the deployment of the E-Invoice is that taxpayers will now receive digitally signed, digitally readable, and traceable invoices as recipients.

1. Building efficient processes

All suppliers must submit data following the required standard under the E-invoice mandate. One of the fundamental requirements for any operation to be automated is the presence of data in a standard format.

As a recipient of standard E-Invoices, you can now automate the recording of purchase invoices in accounting systems, which can increase data accuracy and efficiency.

2. Getting better reconciliation results

Matching the purchase register with GSTR 2B is a critical activity that taxpayers need to do, for accurate claims. One of the biggest challenges in reconciliation has been to identify comparable invoices because the invoice number recorded in the purchase register is not the same as the invoice number provided by the supplier.

With E-Invoices, this challenge can be easily overcome if IRN is used as the base for finding comparable invoices. For this to happen, the IRN needs to be tagged /stored in the Books of accounts of the recipient.

Some gaps to be addressed

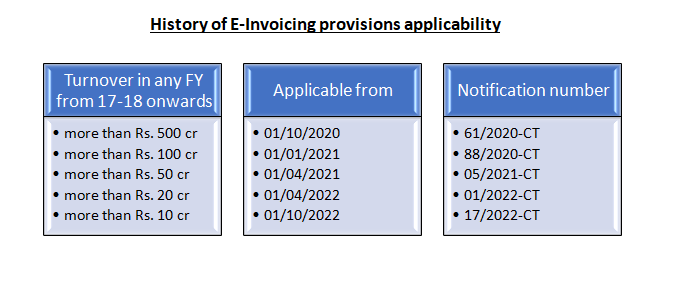

E-invoicing provisions apply to the notified class of taxpayers and transaction types. Irrespective of the fact that whether the data gets auto-populated or not, there are certain challenges and gaps which need to be addressed:

- Invoice data is editable after IRN generation

IRN is made up of the Supplier’s GSTIN, Invoice Number, Document Type, and Financial Year. Post generation of IRN, the invoice could be edited while filing GSTR 1, that edited data of GSTR 1gets reflected in GSTR 2B. This results in differences between the actual invoice and the auto-populated GSTR 2B. Such differences will be identified only after the detailed matching of all invoice fields.

- IRN will not be available on all purchase invoices

For invoices from suppliers that are not subject to the E-Invoice mandate, IRN will not be accessible. Taxpayers should think about calculating IRN using the government’s published reasoning and consistently recording all purchase transactions. This will guarantee a reconciliation process that can be applied consistently to all purchase entries.

Complete automation may also be difficult to achieve if IRN is unavailable. Given that E-Invoice is a national standard, taxpayers may require their vendors to prepare invoices by E-Invoice even if IRN is not to be generated by them as part of their procurement terms and policies.

Conclusion

E-invoicing is a concept that has benefits for all parties involved, including suppliers, beneficiaries, and the government. It opens the avenues to provide value-added solutions and services by using the highest standard, processable and recent invoice data. The mandate currently applies to the notified taxpayers and specified transaction types. Hence not all vendors are under the purview of the E-Invoicing mandate and not all data may be available in a standard format.

So, has it become easier for the purchasers to claim ITC based on the invoices being received from the corresponding suppliers containing the IRN and QR code, or has it increased another check to be complied with before claiming the ITC?

This content is meant for information only and should not be considered as advice, legal opinion, or otherwise. AKGVG & Associates does not intend to advertise its services through this.

Posted by

CA Tarun Kapoor

AKGVG & Associates