The primary focus of every economy has been on increasing the ease of doing business for its people. To achieve this, various relaxations have been given to businesses so that they can put their efforts and resources on their core profit-generating activities rather than getting trapped in the burden of compliances despite having a low turnover. For example, in GST, there is no requirement of registration for suppliers having aggregate turnover in a financial year not exceeding the threshold limit as specified under Section 22 of CGST Act, 2017.

Under GST, the liability of registration arises for every supplier to get himself registered in the State or Union territory from where he makes a taxable supply of goods or services or both, having aggregate turnover in a financial year exceeding the threshold limit.

So, a question might crop up in the minds of the readers, that whether a supplier being duly registered in a State proposing to supply goods or services in some other states will require registration in such other states albeit the said supplier does not have any principal place of business or any fixed establishment in such other states.

This question was discussed primarily by the Karnataka, Authority for Advance Ruling (AAR) in the case of “Re M/s T & D Electricals”

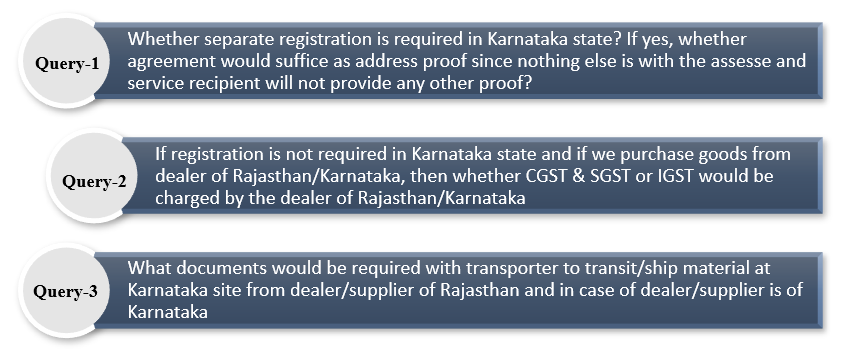

Facts of the case: M/s T & D Electricals (hereinafter referred to as the applicant) is registered as a works contractor and wholesale supplier in Rajasthan. They have been awarded a works contract by M/s Shree Cement Limited at the township in Karnataka (a unit of Shree Cement Ltd.). The applicant had sought an advance ruling as an unregistered person (in the state of Karnataka) in respect of the following questions:-

In view of the query raised by the applicant, the Authority for Advance Ruling (‘AAR’) passed the following ruling:

In response to Query-1

As per Law: Section 22 of CGST Act, every supplier shall be liable to be registered in the State or Union territory from where he makes a taxable supply of goods or services or both if his aggregate turnover in a financial year exceeds the threshold limit.

As per the Case: In the instant case, the applicant is registered in Rajasthan. The applicant was awarded a work contract in the state of Karnataka. However, the applicant does not have any premises or establishment of his own in Karnataka. The applicant holds only one principal place of business, which is in Rajasthan and registration has been obtained for the same. The applicant has no other fixed establishment than the principal place in Rajasthan. Since the applicant intends to supply goods or services or both from the principal place of Rajasthan only, it shall be considered as the location of the supplier and thus no separate registration is required in the state of Karnataka.

Nutshell: The applicant need not obtain separate registration in Karnataka to execute the project in Karnataka. Although, they have the option to obtain the registration if they are capable & intend to have a fixed foundation at the site of the project in Karnataka.

In response to Query-2

As per Law: As per section 10(1)(b) of IGST Act i.e., Bill to Ship to supply, where the goods are delivered by the supplier to a recipient or any other person on the direction of a third person, before or during movement of goods, it shall be deemed that the said third person has received the goods and the place of supply of such goods shall be the principal place of business of such third person.

As per the Case:

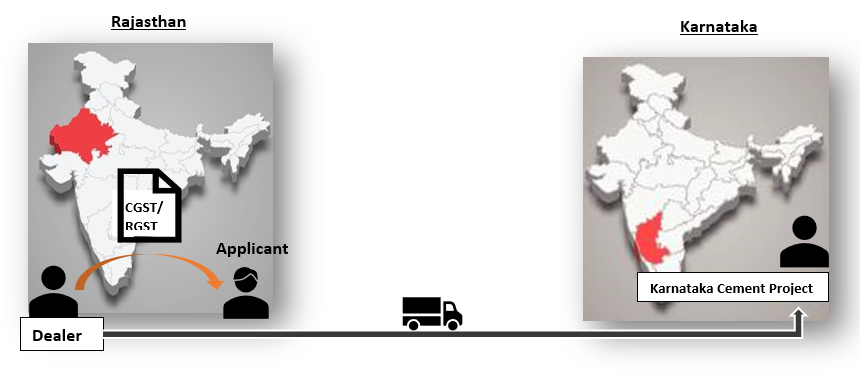

Where inputs/goods are purchased from a dealer of Rajasthan

Dealer of inputs is located in Rajasthan and has supplied goods to Karnataka Cement Project (unit of Shree cement) on the direction of the applicant. Since the location of the supplier (the dealer) is Rajasthan and the place of supply is where the third person(applicant) is located which is also Rajasthan.

Nutshell: Hence supply will be Intra-state supply and thus CGST and RGST shall be applicable

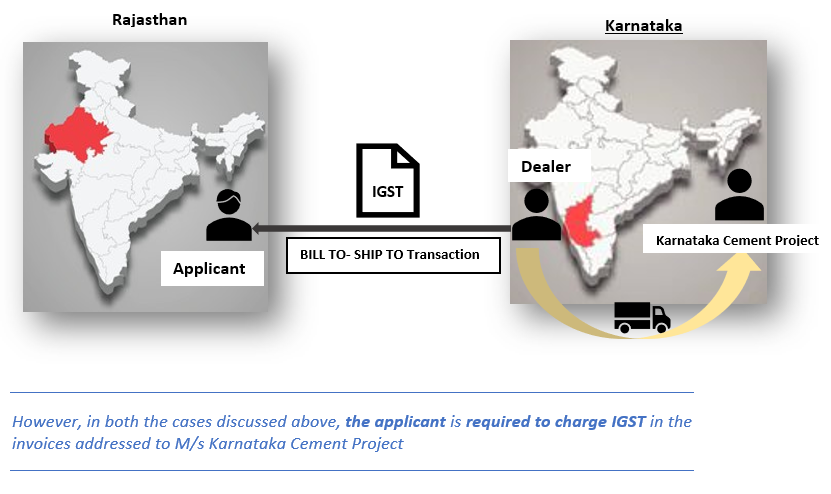

Where inputs/goods are purchased from a dealer of Karnataka

Location of the supplier is located in Karnataka from where he directly supplied inputs to M/s Karnataka Cement Project (a unit of Shree cement) under the direction of a third person i.e. applicant who is located in Rajasthan. So, the location of the supplier is Karnataka, and the place of supply is Rajasthan.

Nutshell: Hence the supply will be Inter-state supply and thus IGST shall be applicable.

Query-3

As per Law: Section 97 states that an applicant desirous of obtaining an advance ruling may make an application in a prescribed manner stating the question on which the advance ruling is sought. The question shall be in respect of cases covered under subsection (2)

As per the Case: The question on documents required to be carried by the transporter of goods does not get covered under the issues on which the advance ruling can be sought.

Nutshell: Thus, no ruling is given on this question as it does not gets covered under Section 97(2) of the CGST Act 2017.

In light of the above rulings pronounced by AAR Karnataka, it can be concluded that a works contract supplier (Applicant) need not get registered in all such states in which he is executing his services.

As a result of the above outcome, there will be fewer compliance requirements on the part of the supplier as he is not required to file the extra GST returns and spend extra rupees for professional charges. It will also lead to a seamless flow of credit to the parties in the transaction. The reduced burden of compliances and cost-saving will ensure that the businesses are on their path of achieving the desired profits by not getting stuck under the unnecessary hurdles which add up to the burden.

This content is meant for information only and should not be considered as an advice or legal opinion, or otherwise. AKGVG & Associates does not intend to advertise its services through this.

Posted by:

CA Tarun Kapoor

AKGVG & Associates